Workers compensation insurance new hampshire

Workers' compensation insurance in New Hampshire is a crucial protection for both employees and employers, ensuring medical benefits and wage replacement for workers injured on the job.

Under state law, most businesses with one or more employees are required to carry this coverage, promoting a safer and more secure work environment. New Hampshire’s workers’ compensation system operates on a no-fault basis, meaning employees can receive benefits regardless of who caused the injury.

This insurance not only supports injured workers during recovery but also shields employers from costly lawsuits. Understanding coverage requirements, claims processes, and compliance regulations is essential for businesses operating in the state.

Florida workers' compensation insurance

Florida workers' compensation insuranceUnderstanding Workers' Compensation Insurance in New Hampshire

Workers' compensation insurance in New Hampshire is a mandatory coverage designed to protect both employees and employers in the event of work-related injuries or illnesses.

This type of insurance provides medical benefits, wage replacement, and rehabilitation services to workers who suffer job-related injuries, ensuring they receive necessary care without resorting to litigation. In New Hampshire, the Workers' Compensation Board oversees the program and enforces compliance with state laws.

Employers with one or more employees, whether full-time, part-time, or seasonal, are generally required to carry workers' comp coverage. Failure to comply can result in significant fines, penalties, and liability for unpaid benefits. Insurance can be obtained through private carriers, the New Hampshire Insurance Alliance (a pool for high-risk businesses), or, in rare cases, through self-insurance approval from the state.

The system promotes a no-fault approach, meaning employees do not need to prove employer negligence to receive benefits, and in return, employers are typically protected from civil lawsuits related to workplace injuries.

Quote workers compensation insurance

Quote workers compensation insuranceWho Needs Workers' Compensation Insurance in New Hampshire?

In New Hampshire, almost all employers with one or more employees are legally required to carry workers' compensation insurance, regardless of whether the employee works full-time, part-time, or seasonally.

This includes corporations, partnerships, and limited liability companies. There are limited exceptions, such as sole proprietors without employees, certain agricultural workers under specific thresholds, and some domestic workers.

However, even in exempt categories, employers may choose to obtain coverage voluntarily for added protection. Independent contractors are generally not covered under an employer’s policy, but the definition of an independent contractor is closely scrutinized to prevent misclassification.

Employers found without proper coverage risk penalties of up to $1,000 per day of noncompliance, in addition to being held fully liable for medical and indemnity costs if an injury occurs.

Railroad workers compensation insurance

Railroad workers compensation insuranceWhat Benefits Does Workers' Compensation Provide in New Hampshire?

Workers' compensation in New Hampshire offers several key benefits to injured employees, including medical treatment coverage, temporary total disability (TTD) benefits, permanent partial disability (PPD) benefits, and vocational rehabilitation services.

Medical benefits cover all reasonable and necessary treatments related to the work injury, from doctor visits to surgery and medications, without employee co-pays.

If an employee is unable to work due to injury, they may receive TTD payments, typically amounting to two-thirds of their average weekly wage, subject to state minimums and maximums. For lasting impairments, PPD benefits are paid based on a statutory schedule that assigns values to different types of injuries.

In cases where a worker cannot return to their previous job, the program may fund retraining through vocational rehabilitation. Additionally, survivors of workers who die from job-related causes may receive death benefits, including burial expenses and ongoing payments to dependents.

Plumbing workers compensation insurance

Plumbing workers compensation insuranceHow to Obtain Workers' Compensation Coverage in New Hampshire

Employers in New Hampshire can obtain workers' compensation insurance through licensed private insurance carriers, which offer competitive policies based on industry risk, payroll size, and safety history.

For businesses that cannot secure coverage in the standard market—often due to high injury rates or being in a high-risk industry—options include the New Hampshire Insurance Alliance (NHIA), which functions as a shared market pool. Employers may also apply for self-insurance status if they meet strict financial and administrative requirements set by the state, including posting a substantial surety bond or letter of credit.

Once insured, employers must display a notice informing employees of their rights under workers' comp law and provide the insurer’s details. Insurance providers are required to file policy information with the New Hampshire Department of Insurance, which conducts audits to ensure compliance with state mandates.

| Benefit Type | Description | Key Details in NH |

|---|---|---|

| Medical Benefits | Covers treatment for work-related injuries or illnesses. | No cost to employee; includes doctor visits, hospitalization, prescriptions, and therapies. |

| Temporary Total Disability (TTD) | Wage replacement for employees unable to work during recovery. | 66.67% of average weekly wage; paid after a 7-day waiting period; subject to state min/max. |

| Permanent Partial Disability (PPD) | Compensation for lasting impairments after recovery. | Calculated using a statutory schedule based on injury type and body part affected. |

| Vocational Rehabilitation | Support for retraining if worker cannot return to prior job. | Includes job counseling, training programs, and placement assistance. |

| Death Benefits | Payments to dependents of workers who die from work injuries. | Up to 66.67% of average weekly wage for survivors; includes up to $10,000 for burial costs. |

Workers Compensation Insurance in New Hampshire: A Comprehensive Guide

Is workers' compensation insurance mandatory for employers in New Hampshire?

Yes, workers' compensation insurance is mandatory for employers in New Hampshire. Under state law, nearly all employers in New Hampshire are required to provide workers’ compensation coverage for their employees. This requirement applies to businesses with one or more employees, whether full-time, part-time, or seasonal.

Best orlando workers compensation insurance

Best orlando workers compensation insuranceThe law is administered by the New Hampshire Department of Labor, and failure to carry proper coverage can result in significant penalties, including fines and potential criminal charges. Employers can obtain coverage through private insurance carriers, the state’s assigned risk pool, or, in rare cases, through self-insurance approval from the state.

Who Must Carry Workers' Compensation Insurance in New Hampshire?

- Most employers in New Hampshire with at least one employee are legally required to carry workers’ compensation insurance. This includes full-time, part-time, and seasonal workers.

- Corporate officers and sole proprietors may elect to exclude themselves from coverage, but if they choose to include themselves or have other employees, they must comply with the mandate.

- Certain agricultural workers, domestic workers in private homes, religious workers, and independent contractors may be exempt under specific conditions, but employers must carefully verify exemption eligibility to avoid penalties.

What Are the Consequences of Not Having Workers’ Compensation Coverage?

- Employers found operating without required coverage can face fines of up to $1,000 per day for each uninsured employee, as well as potential criminal charges classified as Class B misdemeanors.

- The state may issue an insurance cease and desist order, halting business operations until compliance is achieved.

- Uninsured employers can be held personally liable for employee injury claims, including medical expenses and lost wages, which can result in substantial financial burden.

How Can Employers Obtain Workers’ Compensation Insurance in New Hampshire?

- Employers can purchase policies from licensed private insurance carriers authorized to sell workers’ compensation insurance in the state.

- If an employer is unable to secure coverage in the voluntary market, they may obtain a policy through the National Council on Compensation Insurance (NCCI) assigned risk plan, which ensures availability of coverage.

- Larger employers with strong financial standing may apply for self-insurance status, but this requires approval from the New Hampshire Department of Labor and the posting of a security deposit or bond.

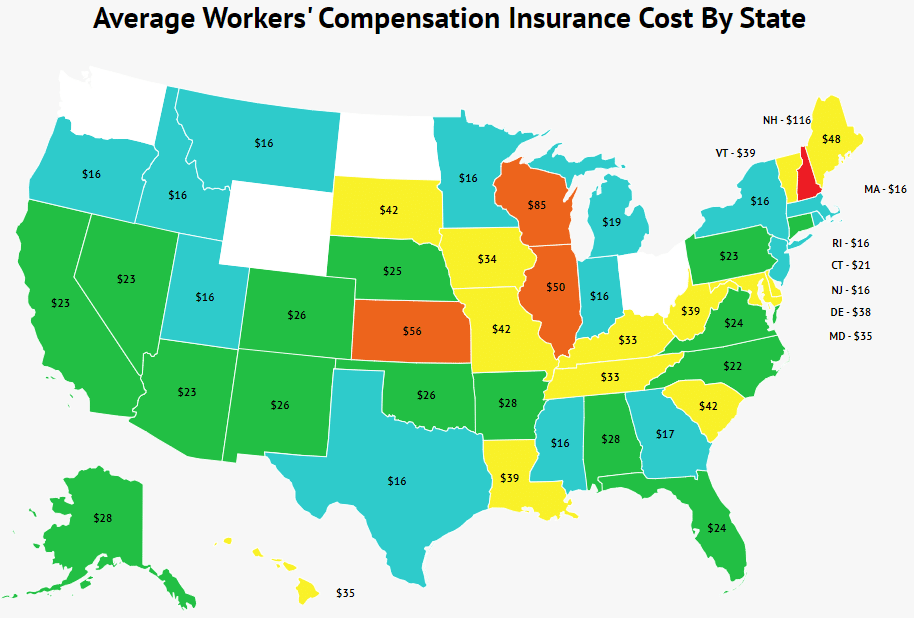

What is the average cost of workers' compensation insurance in New Hampshire?

Typical Cost Range for Workers' Compensation Insurance in New Hampshire

- Workers' compensation insurance costs in New Hampshire typically range from $0.75 to $2.50 per $100 of payroll, depending on the nature of the business and job classifications. This rate is considered relatively competitive compared to national averages, benefiting from the state’s stable insurance market and lower rates of workplace injury in certain industries.

- For small businesses with minimal risk exposure, such as office-based operations or consulting firms, premiums can be quite low—sometimes under $500 annually. On the other hand, high-risk industries like construction, manufacturing, or roofing may pay significantly more due to increased exposure to workplace injuries.

- The actual cost each employer pays is calculated based on a variety of factors, including employee job duties, claims history, total payroll, and workplace safety protocols. Employers are required by state law to carry workers' compensation coverage for all employees, and failure to do so can result in fines and legal action.

- One of the primary factors affecting premiums is the job classification code assigned to each employee. These codes, standardized across the U.S., reflect the risk level associated with specific job duties. For example, an administrative assistant has a lower risk rating than a carpenter, resulting in a lower premium rate.

- Employers with a history of frequent or costly workers’ compensation claims will typically face higher premiums. Insurers use an experience modification factor (mod) to adjust rates based on past claims performance—companies with strong safety records can receive discounts, while those with poor records pay more.

- Payroll size directly impacts total premiums since rates are calculated per $100 of payroll. Larger payrolls naturally result in higher premiums, although economies of scale may allow per-employee costs to decrease slightly as business size increases. Additionally, proper payroll reporting and accurate job classification are critical to avoid audits and unexpected premium adjustments.

How New Hampshire's Market Affects Insurance Pricing

- New Hampshire operates under a competitive workers’ compensation insurance market, where private insurers and the state’s assigned risk pool (the New Hampshire Insurance Underwriting Association) provide coverage. This competition helps keep rates moderate compared to states with monopolistic funds or higher regulatory barriers.

- The state’s relatively low frequency of workers’ compensation claims contributes to stable pricing. Factors such as rigorous safety standards, effective return-to-work programs, and proactive injury prevention efforts help reduce overall claim costs, which benefits both employers and insurers.

- Employers in New Hampshire must obtain coverage from a licensed insurer; self-insurance is allowed for qualified large employers who meet strict financial and reporting requirements. The Department of Labor and the Insurance Department closely regulate the system to ensure compliance and fair treatment of injured workers, which contributes to predictable and transparent pricing.

What is the average cost of workers' compensation insurance in New Hampshire?

The average cost of workers' compensation insurance in New Hampshire typically ranges from $1.25 to $1.75 per $100 of payroll.

This rate can vary significantly depending on the specific industry, the size of the business, the claims history, and the types of job duties employees perform. For example, a low-risk office environment will incur much lower premiums compared to a high-risk construction site.

The state does not mandate a fixed rate, allowing private insurers to set competitive prices under the oversight of the New Hampshire Insurance Department. Employers are required by law to carry workers' compensation coverage if they have at least one employee, whether full-time, part-time, or seasonal.

- Industry classification plays a key role in determining insurance costs, as jobs with higher risks of injury—such as roofing or manufacturing—carry higher premiums due to increased claim likelihood.

- An employer's past claims history affects future rates; businesses with a history of frequent or severe claims will typically face higher premiums through experience rating adjustments.

- The total payroll amount directly influences the overall premium, as insurance is calculated per $100 of payroll, meaning larger payrolls result in higher total insurance costs.

How New Hampshire’s State Regulations Shape Insurance Costs

- The New Hampshire Department of Insurance oversees workers' compensation policies to ensure compliance, fairness in pricing, and adequate coverage for injured workers, which helps maintain a stable insurance market.

- Unlike some states, New Hampshire allows private insurers to compete for business without requiring employers to purchase coverage through a state fund, potentially leading to more competitive rates.

- Mandatory coverage for all employees (including part-time and seasonal workers) ensures broad participation in the system, which can help distribute risk more evenly across employers.

Strategies to Reduce Workers' Compensation Costs in the State

- Implementing comprehensive workplace safety programs can reduce the frequency of accidents and injuries, thereby lowering the risk profile and potentially reducing insurance premiums.

- Conducting regular audits and classifying employees correctly ensures that employers are not overpaying due to incorrect job risk categorizations.

- Working with experienced insurance brokers who understand New Hampshire’s specific regulations and market can help businesses find policies that offer optimal coverage at competitive rates.

What are the key eligibility criteria for workers' compensation in New Hampshire?

Employment Status and Coverage Requirements

In New Hampshire, one of the foundational eligibility factors for workers’ compensation benefits is the worker’s employment status.

The law generally requires that the individual be classified as an employee rather than an independent contractor to qualify for benefits. Most employers in the state are required by law to carry workers’ compensation insurance if they employ one or more workers, whether full-time or part-time.

However, certain categories of workers may be excluded, such as some agricultural laborers, domestic workers, and volunteer workers, depending on the circumstances. It is also important to note that even if an employer fails to carry insurance, injured workers may still be eligible to receive benefits through the state’s Workers’ Compensation Assigned Risk Plan.

- Applicants must be formal employees under a recognized employer-employee relationship

- Employers with at least one employee are typically required to provide coverage

- Independent contractors and some specific worker categories may not be covered under standard policies

Type and Timing of Injury

To be eligible for workers’ compensation in New Hampshire, the injury or illness must arise out of and occur in the course of employment. This means the injury must be directly related to job duties and happen while the worker is performing tasks for their employer.

Injuries that happen during normal commuting are generally not covered, unless the worker is on a special work-related assignment. Additionally, occupational diseases that develop over time due to workplace conditions may also qualify, provided there is a clear link to the work environment.

It is crucial that the injury is reported promptly; workers are required to notify their employer within 14 days of the incident or within 90 days for occupational diseases, to preserve eligibility.

- The injury must have a direct connection to employment duties and occur during work hours or related activities

- Occupational illnesses are covered if causally related to workplace conditions and properly documented

- Timely reporting is mandatory: notice to the employer must be given within 14 days for accidents or 90 days for occupational diseases

Compliance with Reporting and Filing Procedures

Meeting procedural requirements is essential for maintaining eligibility in New Hampshire’s workers’ compensation system.

After notifying the employer of the injury, the employee should ensure that a First Report of Injury is filed by the employer with the insurance carrier and the state. If the claim is disputed or benefits are denied, the worker must act within strict deadlines.

For example, a petition to controvert must be filed within three years from the date of injury to initiate legal proceedings. Medical treatment must generally be authorized through the workers' compensation system, and failure to follow prescribed protocols—such as seeking unauthorized treatment without approval—may jeopardize eligibility.

- Employers must file a First Report of Injury with the insurer and state authorities

- Workers must file a petition within three years of the injury to pursue disputed claims

- Medical care should be obtained through authorized providers to maintain benefit eligibility

Frequently Asked Questions

What is workers' compensation insurance in New Hampshire?

Workers' compensation insurance in New Hampshire provides benefits to employees who suffer work-related injuries or illnesses. It covers medical expenses, lost wages, and rehabilitation costs. Employers are required by law to carry this insurance if they have four or more employees. The program helps protect both workers and employers by ensuring prompt medical care and reducing lawsuits over workplace injuries.

Who needs workers' compensation insurance in New Hampshire?

Most employers in New Hampshire with four or more employees must carry workers' compensation insurance, including full-time, part-time, and seasonal workers. Some exceptions apply, such as sole proprietors and certain agricultural workers. Even businesses with fewer than four employees are encouraged to have coverage. Failure to maintain required insurance can lead to penalties, fines, and legal liability for workplace injury costs.

How do employees file a workers' compensation claim in New Hampshire?

In New Hampshire, employees should report work-related injuries to their employer as soon as possible, preferably in writing. The employer must then notify their insurance provider and file the necessary forms with the state. Employees may need to complete a Claim for Compensation form (Form 31). Seeking medical treatment from an authorized provider and cooperating with the insurer’s investigation helps ensure timely claim processing.

What benefits does workers' compensation provide in New Hampshire?

Workers' compensation in New Hampshire offers medical treatment coverage, wage replacement for lost income, disability benefits (temporary or permanent), vocational rehabilitation, and survivor benefits if a work injury results in death. Wage benefits are typically two-thirds of the employee’s average weekly wage, subject to state limits. All benefits are designed to support recovery and help injured workers return to suitable employment safely.

Leave a Reply