Quote workers compensation insurance

Workers' compensation insurance is a crucial safeguard for businesses and employees alike, providing financial protection in the event of workplace injuries or illnesses.

This type of insurance covers medical expenses, rehabilitation costs, and lost wages for employees who suffer job-related injuries, helping them recover without financial strain. For employers, it reduces the risk of costly lawsuits and ensures compliance with legal requirements.

Obtaining an accurate quote for workers' compensation insurance involves evaluating factors such as industry type, payroll size, and workplace safety history. Understanding these elements helps businesses secure appropriate coverage at competitive rates.

Florida workers' compensation insurance

Florida workers' compensation insuranceHow to Get an Accurate Workers Compensation Insurance Quote

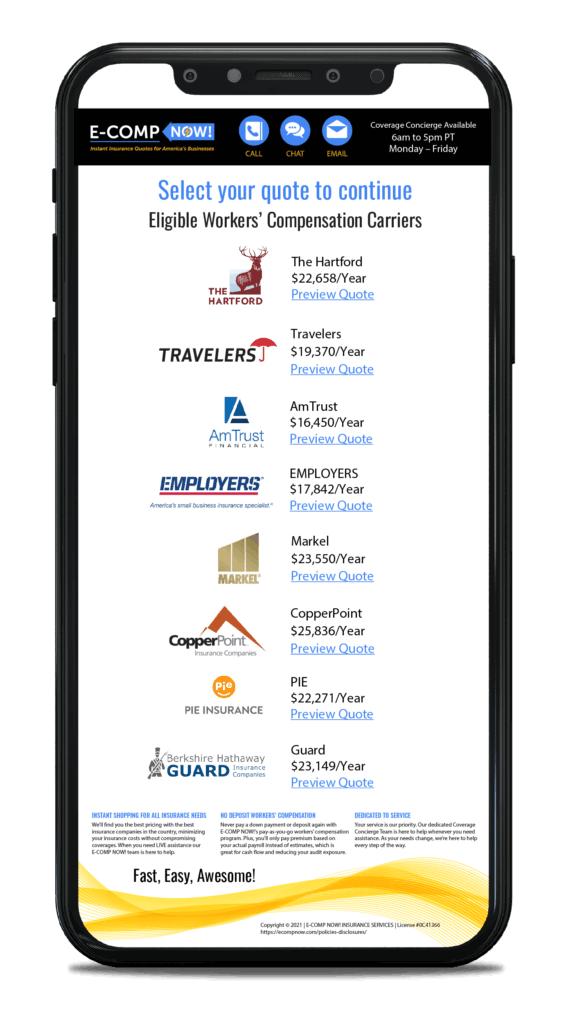

Obtaining a precise workers compensation insurance quote is a critical step for businesses aiming to protect their employees and manage financial risks associated with workplace injuries. This type of insurance covers medical expenses, rehabilitation costs, and lost wages when an employee suffers a work-related injury or illness.

To receive an accurate quote, businesses must provide detailed information about their operations, including employee job classifications, annual payroll, industry type, and historical claims data. Insurance providers use this data to assess risk levels and calculate premiums.

The process typically involves completing a detailed application, after which insurers may conduct workplace evaluations or request additional documentation to finalize the quote. Ensuring transparency and completeness during this stage is essential to avoid underinsurance or unexpected costs later.

Factors That Influence Workers Compensation Insurance Quotes

Several key factors directly affect the cost of a workers compensation insurance quote. The primary determinant is the nature of the business and its associated risk levels—industries with higher physical demands, such as construction or manufacturing, typically face higher premiums due to increased injury risks. Employee job classifications are crucial because insurers assign specific risk codes to different roles, impacting the overall rate.

Railroad workers compensation insurance

Railroad workers compensation insuranceAnnual payroll also plays a significant role, as premiums are often calculated per $100 of payroll. Businesses with a history of frequent or severe claims may experience higher quotes due to poor experience modification ratings (mod rate).

Additionally, geographic location, workplace safety programs, and regulatory standards within a state can further influence insurance costs. Understanding these variables enables employers to proactively manage their risk profile and secure more competitive rates.

How to Compare Different Workers Compensation Insurance Quotes

When comparing workers compensation insurance quotes, businesses should evaluate more than just the premium cost. It's essential to assess the scope of coverage, including what medical treatments, disability benefits, and legal expenses are included. Pay attention to policy exclusions and limitations that might reduce protection in specific situations.

Look for insurers offering strong claims management services, as efficient processing can reduce downtime and improve employee satisfaction. Consider the financial stability and customer service reputation of each provider—ratings from agencies like AM Best can provide insight.

Plumbing workers compensation insurance

Plumbing workers compensation insuranceSome quotes may include added benefits like safety training programs or loss prevention resources, which can reduce future claims. Using a licensed broker or online comparison platform can help you review multiple quotes side-by-side, ensuring you choose a policy that balances affordability with comprehensive protection.

Common Mistakes to Avoid When Requesting a Workers Comp Quote

Many employers make costly errors when seeking a workers compensation insurance quote, which can lead to inadequate coverage or inflated premiums. One common mistake is underreporting payroll or misclassifying employees, which may result in policy cancellations or penalties during audits.

Failing to disclose past claims or workplace hazards can also impact the accuracy of the quote and the insurer’s willingness to pay future claims. Another error is focusing solely on price without evaluating the insurer’s claims handling efficiency or network of medical providers.

Businesses sometimes delay purchasing coverage, leaving them exposed during early operations. Additionally, not reviewing policy details annually or updating classifications as job roles evolve can lead to coverage gaps. Avoiding these pitfalls ensures a smoother quoting process and long-term financial and operational protection.

| Factor | Impact on Quote | Why It Matters |

|---|---|---|

| Employee Classification Codes | High impact – higher risk jobs cost more | Insurers use these codes to assign risk levels; using the wrong code can lead to overpayment or audit penalties. |

| Annual Payroll | Direct proportional impact | Premiums are calculated per $100 of payroll; accurate reporting is required to avoid retroactive charges. |

| Claims History (Mod Rate) | Major influence on pricing | A poor experience mod rate from frequent claims can increase premiums by 20–50% or more. |

| Industry Type | Baseline risk assessment | High-risk industries like roofing or logging face significantly higher base rates than office-based businesses. |

| State Regulations | Varies by location | Each state sets its own rules and rates; location affects both coverage requirements and pricing. |

Frequently Asked Questions

What is workers' compensation insurance?

Workers' compensation insurance provides benefits to employees who suffer work-related injuries or illnesses. It covers medical expenses, lost wages, and rehabilitation costs.

Employers are typically required by law to carry this insurance to protect both employees and the business. The coverage applies regardless of fault, ensuring employees receive timely support while reducing the risk of lawsuits against employers.

Why should I get a quote for workers' compensation insurance?

Getting a quote helps you understand the cost of coverage based on your business size, industry, and risk level. It allows you to compare policies and providers to find affordable, comprehensive protection.

A detailed quote ensures you’re not overpaying and that your policy meets legal requirements. Accurate quotes also prevent coverage gaps, helping safeguard your employees and business from financial loss due to workplace accidents.

How is the cost of workers' comp insurance determined?

The cost is based on several factors, including your industry’s risk level, payroll size, job types, and claims history. Insurers use a rate per $100 of payroll, adjusted for risk class and experience modification.

Safe workplaces with fewer claims often pay lower premiums. Accurate classification of employee roles and proper payroll reporting are essential to avoid overcharging and ensure appropriate coverage for your business needs.

Can I get workers' comp coverage if I’m self-employed or have no employees?

Most states require workers’ comp only if you have employees, so sole proprietors without staff aren’t always required to have it.

However, some self-employed individuals in high-risk fields choose to purchase coverage for protection. Contractors may also need it if requested by clients. While optional in many cases, having coverage can safeguard your finances if a work-related injury occurs, especially in hazardous industries.

Leave a Reply