Best value workers' compensation insurance options

Finding the best value workers’ compensation insurance requires balancing affordability with comprehensive coverage. For businesses of all sizes, this type of insurance is essential to protect employees and employers in the event of workplace injuries.

The most valuable options offer competitive premiums, reliable claims processing, strong customer support, and flexible policies tailored to specific industries. Companies should evaluate insurers based on financial stability, customer reviews, available endorsements, and ease of compliance with state regulations.

While cost is important, the lowest premium doesn’t always provide the best long-term value. Assessing coverage details and service quality ensures businesses get optimal protection without overspending.

Workers compensation insurance new hampshire

Workers compensation insurance new hampshireBest Value Workers' Compensation Insurance Options for Businesses

Finding the best value workers' compensation insurance options means more than just selecting the cheapest policy—it involves identifying a plan that balances cost, coverage breadth, and service quality to meet the unique needs of your business. Value is defined by how effectively the policy protects your employees and your bottom line in the event of workplace injuries.

Employers across industries must evaluate providers based on their claims handling efficiency, premium rates, safety programs, and additional support services. Small and mid-sized businesses, in particular, benefit from policies that offer scalable coverage, loss prevention tools, and flexible payment options.

Engaging with reputable insurers or using a qualified broker can help organizations compare multiple plans side by side, ensuring they maximize benefits without overpaying. Ultimately, the best value lies in securing comprehensive protection that reduces long-term financial risks and promotes a safer workplace.

Key Factors That Determine the Value of Workers' Comp Insurance

When assessing the value of workers' compensation insurance, several critical factors come into play, including industry risk classification, company claims history, payroll size, and state regulations.

California workers compensation insurance cost 2025

California workers compensation insurance cost 2025Insurers use these metrics to calculate premiums, but value goes beyond the price tag—efficient claims management, access to a broad medical provider network, and strong return-to-work programs can greatly enhance a policy’s worth. Businesses with strong safety records may qualify for experience modification discounts, significantly lowering long-term costs.

Additionally, insurers offering proactive loss control services and safety training can reduce injury rates and, consequently, future premiums. Understanding these variables allows employers to evaluate which plans deliver the most robust protection for the investment, ensuring both regulatory compliance and financial protection.

Top Providers Offering Competitive and Comprehensive Coverage

Several insurers stand out for offering best value workers' compensation insurance options due to their combination of affordability, reliability, and customer support. Companies like Nationwide, The Hartford, and Progressive Workers Comp are frequently recognized for their tailored solutions, fast claims processing, and suite of risk management tools.

These providers often offer online portals for policy management, real-time reporting, and safety resources that empower businesses to reduce workplace incidents. Some also feature pay-as-you-go premium models, aligning costs with actual payroll and improving cash flow for seasonal or growing businesses. Below is a comparison of leading insurers based on key value indicators:

Best workers compensation insurance for small businesses 2025

Best workers compensation insurance for small businesses 2025| Insurance Provider | Claims Service Rating | Premium Flexibility | Additional Value Features |

|---|---|---|---|

| The Hartford | Excellent | Pay-as-you-go and standard options | 24/7 claims support, robust safety training |

| Nationwide | Very Good | Standard pricing with experience mods | Dedicated risk consultants, mobile claims app |

| Progressive | Excellent | Pay-as-you-go availability | Fast claim payments, user-friendly platform |

| Travelers | Excellent | Flexibility with large accounts | Advanced data analytics for risk reduction |

How Small Businesses Can Maximize Cost Efficiency

For small businesses, maximizing cost efficiency in workers’ comp insurance requires strategic planning and proactive risk management. One of the most effective ways to reduce premiums is by maintaining a safe work environment through regular employee training, clear safety protocols, and routine equipment maintenance, all of which lower the likelihood of workplace injuries.

Implementing a formal safety program can also qualify businesses for premium discounts or dividend incentives from insurers. Another cost-saving strategy is to audit payroll classifications to ensure employees are categorized correctly—misclassification can lead to overpayment.

Choosing a policy with loss-sensitive rating plans, such as a retrospective premium program, can also deliver long-term savings for businesses with excellent loss histories. By focusing on prevention and accurate reporting, small businesses can significantly improve the value they receive from their workers' compensation coverage.

Best Value Workers' Compensation Insurance Options: A Comprehensive Guide

What are the top value workers' compensation insurance options available?

Best workers' compensation insurance for small businesses 2025

Best workers' compensation insurance for small businesses 2025Top National Providers with Competitive Rates and Comprehensive Coverage

- Travelers is consistently ranked among the top workers' compensation insurers due to its financial strength, extensive network of safety resources, and risk management support. The company offers customizable policies for businesses of all sizes and provides industry-specific solutions that help reduce claims and premiums over time.

- Liberty Mutual is another major national insurer known for competitive pricing and strong claims handling. They offer proactive injury prevention programs and real-time claims tracking tools, helping employers stay informed and reduce lost workdays. Their large scale allows them to spread risk efficiently, often resulting in favorable rates.

- Chubb combines financial stability with tailored underwriting, making it a preferred option for mid-sized and larger companies seeking both coverage and risk consultation. Chubb emphasizes loss prevention services and provides access to safety engineers, which can lead to fewer workplace incidents and lower long-term costs.

State-Run and Monopolistic Workers' Comp Programs

- In certain states like Ohio, Washington, North Dakota, and Wyoming, workers’ compensation insurance is only available through state-run funds. These monopolistic state funds eliminate competition but often offer stability, predictable pricing, and inclusive coverage regardless of a company’s claims history. For businesses operating in these states, enrollment in the state program is mandatory.

- The Washington State Department of Labor & Industries (L&I) provides fully funded, no-fault insurance that covers medical care, lost wages, and rehabilitation. Employers contribute based on their industry’s risk classification and safety record, with incentives for maintaining safe workplaces.

- Ohio’s Bureau of Workers’ Compensation (BWC) offers additional loss prevention services, safety consultations, and premium discount programs for companies that demonstrate strong safety practices. Although employers cannot choose private carriers in these states, the state funds often reinvest in workplace safety, which can reduce overall claim frequency.

Small Business and Alternative Group Insurance Solutions

- Progressive Commercial offers workers’ comp options specifically designed for small businesses, particularly in industries like construction, janitorial services, and transportation. Their focus on digital tools for reporting and managing claims makes administration easier for small employers with limited HR staff.

- Insureon connects small businesses with multiple A-rated carriers through an online platform, allowing side-by-side comparisons of pricing and coverage terms. This digital brokerage model increases accessibility and helps small companies find the most value-driven policies without long sales cycles.

- Group self-insurance pools and trade association plans are alternative options where similar businesses pool resources to cover claims collectively. These groups often benefit from lower administrative costs and shared risk management practices, offering favorable value especially in high-risk industries where traditional premiums may be prohibitive.

What are the most cost-effective workers' compensation insurance options for minimizing expenses?

Shop Around and Compare Multiple Carriers

One of the most effective ways to reduce workers' compensation insurance costs is to actively seek quotes from multiple insurance providers.

Different carriers use varying risk assessment models, claims histories, and rating systems, leading to significant price differences for the same business. By comparing policies, businesses can identify the most competitive rates while ensuring adequate coverage.

- Request detailed quotes from at least three to five authorized workers' comp insurers operating in your state.

- Use independent insurance brokers who have access to multiple carriers and can negotiate on your behalf.

- Regularly re-bid your policy every renewal period, as market conditions and carrier pricing strategies may shift over time.

Implement and Maintain a Strong Safety Program

Insurance premiums are heavily influenced by a company’s claim history, and maintaining a safe workplace directly reduces incidents and subsequent claims. Insurers often offer premium discounts to businesses with proven safety programs, as fewer claims translate into lower risk for the insurer.

- Develop written safety protocols tailored to your industry and conduct regular employee training sessions.

- Assign designated safety officers to monitor compliance and perform routine hazard assessments.

- Encourage prompt reporting of near-misses and minor incidents to prevent future serious claims, potentially improving your experience modification rate (EMR).

Classify Employees Correctly and Review Payroll Reporting

Accurate employee classification and payroll reporting are critical for avoiding overpayment on premiums. Workers are categorized into class codes based on job risk levels, and misclassification can significantly inflate costs. Similarly, reported payroll directly affects premium calculations, so errors here can lead to unnecessary expenses.

Wisconsin workers compensation insurance employer requirements

Wisconsin workers compensation insurance employer requirements- Audit job duties annually to ensure each employee is assigned the correct class code as defined by your state’s rating bureau.

- Separate administrative staff from high-risk laborers in payroll reporting to apply lower rates where applicable.

- Verify that subcontractors carry their own workers’ compensation coverage to avoid including their payroll in your premium calculations.

What is the ideal cost for high-value workers' compensation insurance coverage?

Factors Influencing the Ideal Cost of Workers' Compensation Insurance

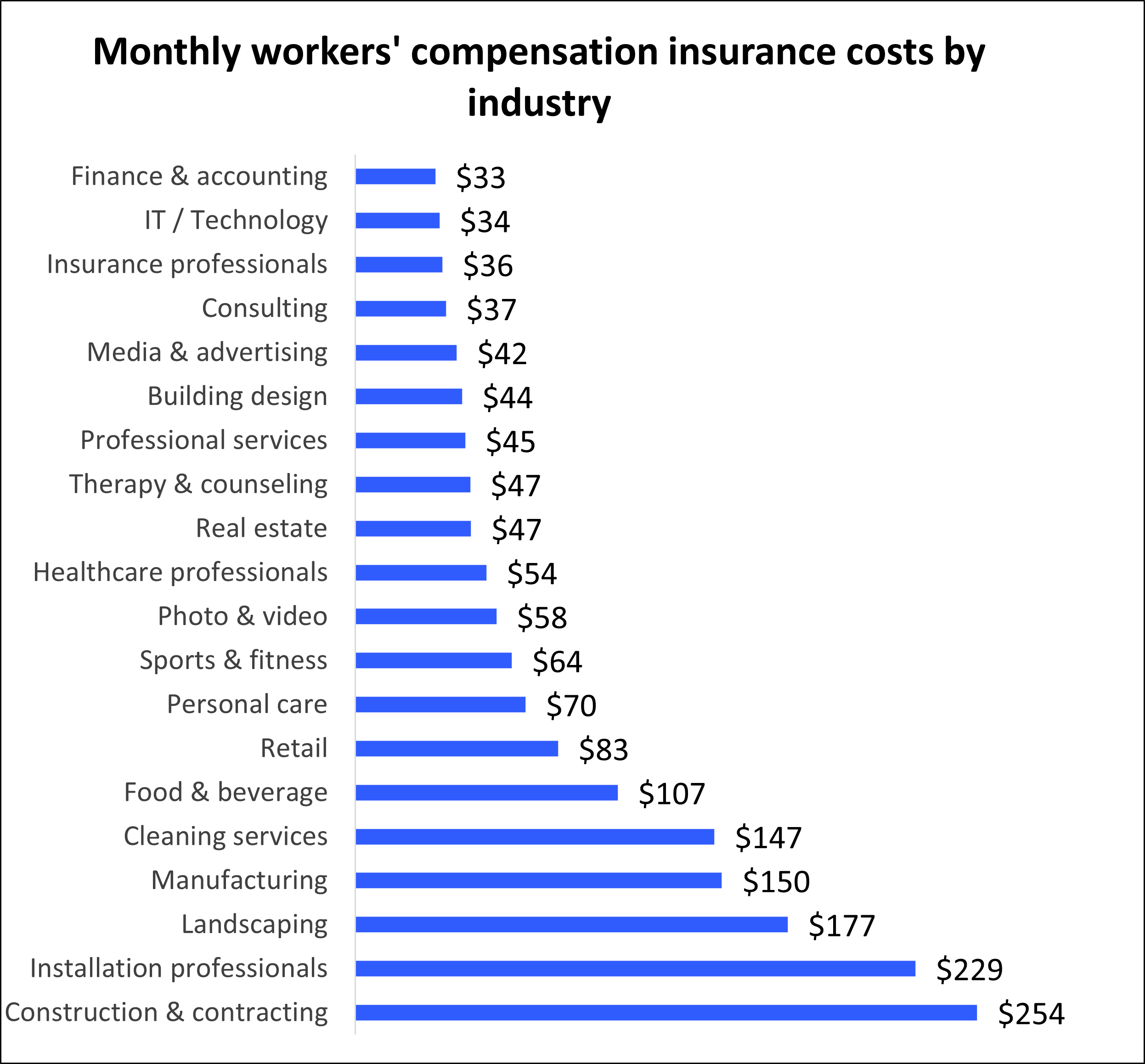

- The ideal cost of high-value workers' compensation insurance is influenced by several key factors, including the nature of the industry, job classifications, and the company’s claims history. High-risk sectors such as construction, manufacturing, or transportation typically face higher premiums due to increased likelihood of workplace injuries.

- Location also plays a significant role, as insurance regulations and average medical costs vary from state to state. For instance, states like California and Texas have different rating systems and legal environments that directly impact premium amounts.

- Additionally, a company's past claims experience—often summarized in an experience modification factor (mod factor)—can either increase or reduce the final cost. Businesses with fewer claims and strong safety programs often qualify for lower rates, moving closer to what might be considered an ideal cost relative to their risk exposure.

- When evaluating the ideal cost, businesses should compare their premiums against industry benchmarks. The national average for workers’ compensation insurance is typically between $0.50 and $2.00 per $100 of payroll, but high-value coverage for specialized or high-risk roles can exceed $5.00 per $100 in premium costs.

- The scope and depth of coverage also affect pricing. High-value policies may include broader benefits, higher indemnity limits, or coverage for non-traditional work arrangements, which justify elevated premiums but also offer greater financial protection.

- Working with a knowledgeable broker to analyze rate proposals from multiple carriers helps identify competitive pricing. Transparency in how rates are calculated—such as class codes, payroll estimates, and safety discounts—enables employers to pinpoint what constitutes a fair and ideal cost for their specific circumstances.

Strategies to Achieve a Competitive and Sustainable Cost

- Implementing comprehensive workplace safety programs is one of the most effective ways to control and reduce insurance costs over time. Companies that invest in training, equipment maintenance, and injury prevention protocols often see a direct reduction in claims frequency and severity, leading to lower premiums.

- Regularly auditing payroll and job classifications ensures that employers are not overpaying due to misclassification. Accurate categorization of employees by risk level can prevent overcharging and align premiums more closely with actual exposure.

- Participating in dividend or experience-rated programs allows eligible businesses to receive rebates if they maintain low claim levels. These programs reward responsible risk management and help balance out the cost of high-value coverage, making it more sustainable in the long term.

What should you avoid saying when discussing workers' compensation insurance options?

Don't Downplay the Importance of Coverage

Minimizing the significance of workers' compensation insurance can undermine its value and discourage employees from understanding their rights and protections.

It is critical to communicate that this insurance serves as a safeguard for both employers and employees in the event of workplace injuries. Dismissing it as unnecessary or overly bureaucratic can create a false sense of security and lead to poor decision-making.

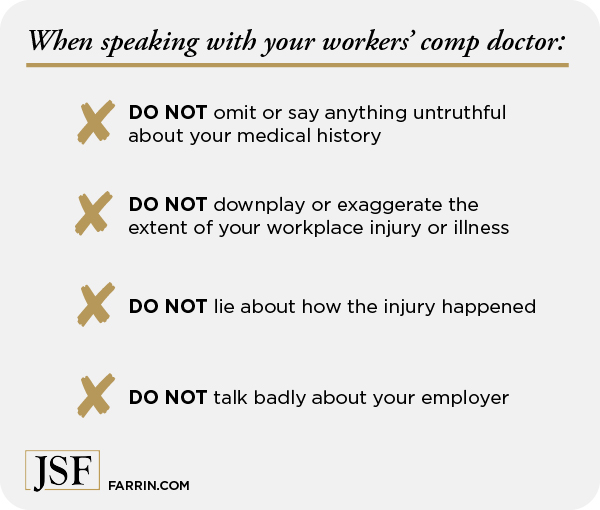

- Never say, We’ve never had an injury, so we don’t need full coverage, as it ignores the unpredictable nature of workplace accidents and may result in severe financial and legal consequences if an incident occurs.

- Avoid suggesting that claims are rare or exaggerated, as this can erode trust and make employees hesitant to report legitimate injuries, potentially violating safety regulations.

- Do not frame workers' comp as a financial burden rather than a legal and ethical responsibility, because this shifts focus away from employee well-being and organizational accountability.

Avoid Discouraging Claims or Suggesting Retaliation

Creating an environment where employees fear consequences for filing a workers' compensation claim is not only unethical but also illegal. Any comment that implies disapproval of claims can discourage injured workers from seeking necessary medical care and reporting incidents promptly, which can escalate costs and expose employers to penalties.

- Never state, If you file a claim, it might affect your job, as this implies retaliation and violates federal and state anti-retaliation laws designed to protect workers.

- Do not say things like, Other companies don’t have this many claims, which can make employees feel guilty or stigmatized for getting hurt on the job.

- Avoid comments such as, We’ll have to raise insurance costs because of you, as they place blame on the injured worker and discourage transparency in workplace safety reporting.

Don't Misrepresent Policy Details or Legal Obligations

Providing inaccurate information about coverage terms, eligibility, or legal requirements can lead to confusion, non-compliance, and potential liability. Workers' compensation laws vary by jurisdiction, and misstatements may result in employees missing out on benefits or employers facing regulatory action.

- Do not claim, You won’t get paid during recovery, because most policies provide some form of wage replacement, and such misinformation may prevent employees from seeking rightful benefits.

- Avoid saying, You can only claim if someone else was at fault, since workers' comp is typically a no-fault system, meaning employees are covered regardless of who caused the injury.

- Never state, We can opt out of workers' comp legally, without clarifying state-specific mandates, as most states require coverage for nearly all employers, and this could encourage non-compliance.

Frequently Asked Questions

What makes a workers' compensation insurance option the best value?

The best value workers' compensation insurance offers reliable coverage at a competitive price, with strong financial ratings and excellent claims support. It balances affordability with comprehensive protection, minimizing out-of-pocket costs after workplace injuries.

Value also includes responsive customer service, online tools for managing policies, and loss prevention programs that reduce future claims and lower long-term premiums for businesses.

How can small businesses find affordable workers' comp insurance without sacrificing coverage?

Small businesses can find affordable, high-value workers' comp insurance by comparing quotes from multiple reputable insurers and working with experienced brokers.

Maintaining a safe workplace reduces claims and premiums. Businesses should also take advantage of state-mandated discounts, participate in safety programs, and consider pay-as-you-go plans that align premiums with payroll, improving cash flow while ensuring full coverage for all employees.

Are state funds or private insurers better for cost-effective workers' compensation?

Both state funds and private insurers can offer cost-effective workers' comp, depending on your location and risk profile. State funds often provide stable rates and guaranteed coverage, especially for high-risk industries.

Private insurers may offer more flexible terms and additional benefits like safety training or lower premiums for excellent loss history, making them competitive choices for low-risk or safety-conscious businesses seeking better overall value.

What discounts or programs help reduce workers' comp insurance costs?

Common discounts include experience modification credits, safety program incentives, and bundling policies with the same insurer.

Employers who invest in workplace safety training, return-to-work programs, and injury prevention may qualify for reduced rates. Some insurers also offer pay-as-you-go plans, audits to correct payroll overestimations, and group policies through trade associations, all of which can significantly lower premiums while maintaining strong employee protection.

Leave a Reply